Client centricity is critical to surviving and succeeding in the retail landscape, which is extra turbulent than ever.

This report works by using EDITED’s Organization Intelligence info to navigate how shopper behavior is evolving and assistance stores modify their tactics accordingly.

Continue to keep reading for insights and reach out for a totally free demo to see our info in motion.

Key Takeaways

-

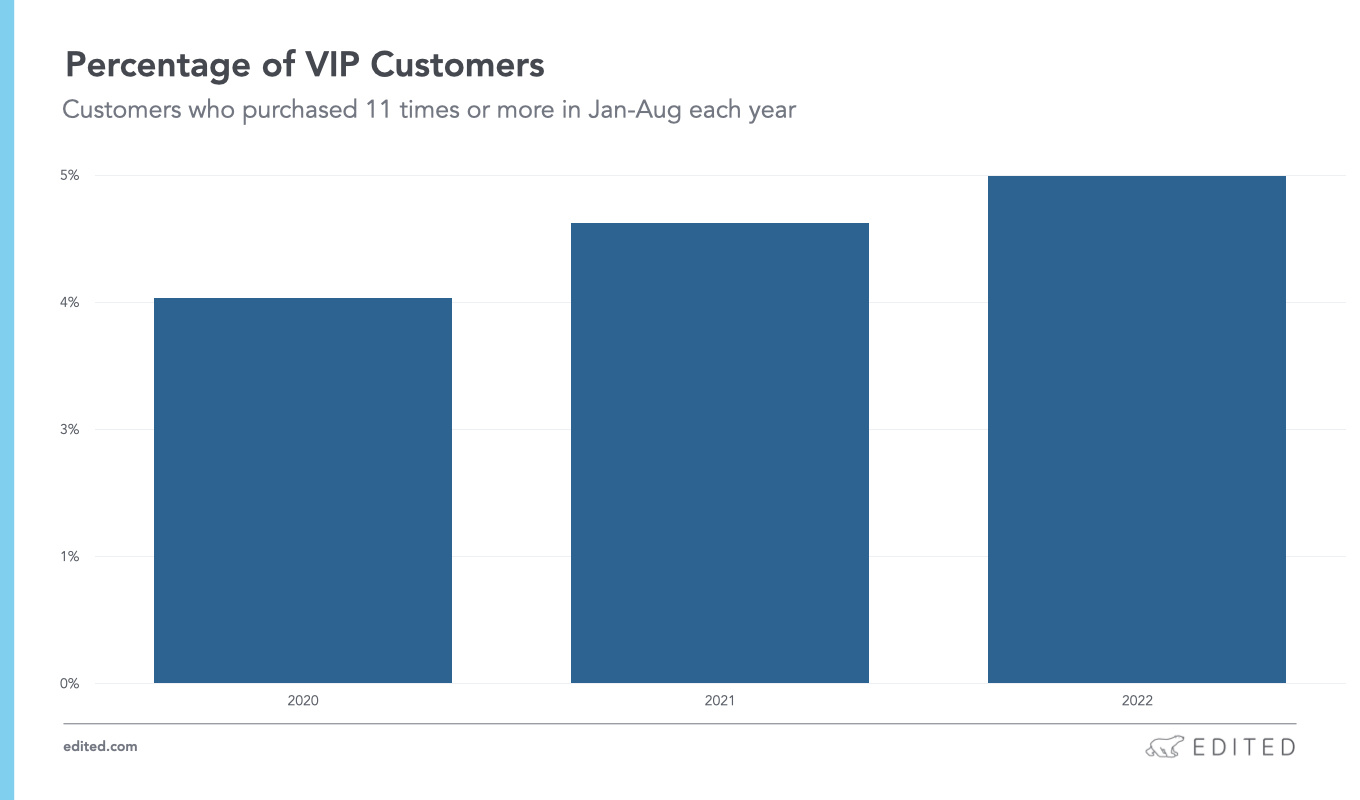

Brand loyalty continues to be at a two-calendar year substantial, with VIPs growing from 4.53% to 5% YoY of overall consumers. New prospects seem to be significantly less self-confident buying outside their favored vendors as the price tag of dwelling disaster accelerates, dropping 3pp YoY from the whole team.

-

The average shopper profitability for VIPs dipped over the past 3 months, a pattern in line with 2021. In the meantime, profit for each buy for new shoppers rose by $6 YoY, highlighting the likely of diversifying viewers get to.

-

The rising price of dwelling has led to individuals getting more conservative with buys, a bit pulling back on units per get from 2.91 in 2021 to 2.88 for each. Inflation also led to ordinary purchase values raising by $11 (6%) YoY, incorporating to cautious shelling out.

-

Suppliers are continue to going through difficulties across the benefit chain, with unsold stock amounts above the past a few months obtaining risen from 15% in 2021 to 18%, when yr to day, return rates are 3pp larger than in 2020.

Are Buyers Becoming A lot less Faithful?

Retailers’ provide chains are continue to less than strain, major to delays in dispatching goods to customers. When stabilizing considering that a backlog in January, which saw average shipping occasions almost climb to 4 days, deliveries are nevertheless slower than very last calendar year, averaging at 2.7 days YTD vs. 2.4 in 2021.

Even with this, VIP clients have remained additional loyal than ever to their preferred models during the year. This cohort accounts for purchasers who have obtained from a retailer 11 moments or additional and equals 5% of the whole purchaser portfolio, up from 4.53% in 2021, and is a two-calendar year high.

Meanwhile, shops are battling to entice new clients, who might be considerably less self-assured browsing outdoors their experimented with-and-analyzed brand names if they are going through financial anxiety due to the price tag of dwelling crisis. Initially-time purchasers have found a downward trajectory because the outbreak of COVID in 2020, and this client group dropped 3pp from 31% to 28% of on the net shoppers YoY.

Are Shoppers Acquiring Extra?

Due to the fact the start out of the 12 months, inflation throughout transport and raw resources has seen common get values enhance $11 (6%) YoY. These prices climbing alongside residing fees have led to consumers pulling back a bit on order quantities, with models for every buy averaging 2.88 per get vs. 2.91 in 2021.

Yr to day, there has been a sample of each new and repeat customers paying additional YoY. VIPS have been the most rewarding cohort, having to pay $12.26 (16%) a lot more, when new clients are paying $10.70 (13%) a lot more YoY.

However, we’re beginning to see a shift – over the earlier a few months, the normal profit for each buy for new customers YoY has enhanced by $6 on 2021, although remaining relatively flat for VIPs, underscoring the importance of participating clean audiences which, although are declining YoY, have the possible to be investing additional.

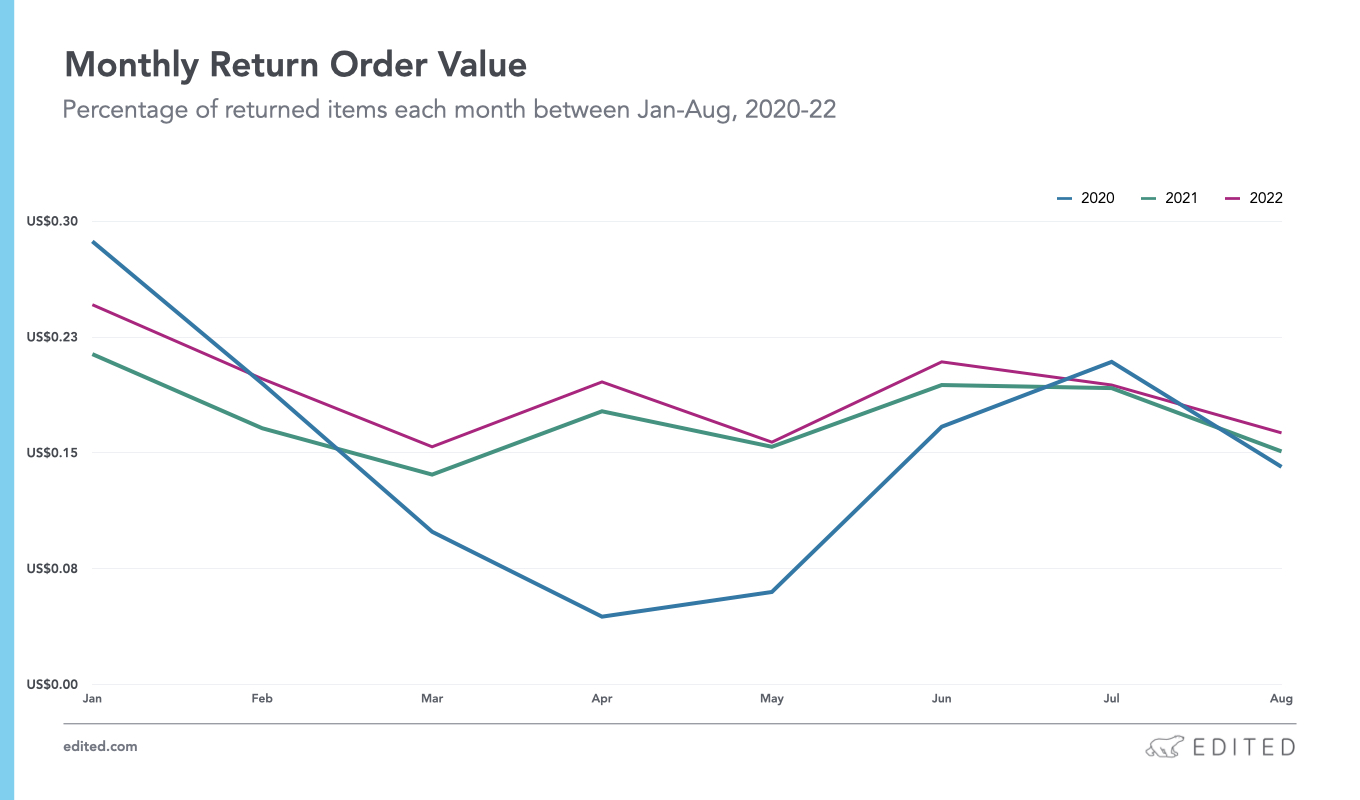

Are Shoppers Returning A lot more Merchandise?

Return rates saw their regular spike at the begin of the year and then outpaced 2021 and 2022 in April and June. Higher returns have eased as the price tag of dwelling disaster, coupled with vendors charging for returns, have led to prospects producing much more conscious buying selections. Nonetheless, they are still at a two-yr record of 18.96% YTD.

Merchants are nevertheless plagued by source chain difficulties, apparent by the glut of unsold products. More than the earlier 3 months, deadstock reached an regular of 18% vs. 15% in 2021, which could be due to a blend of deliveries not arriving on time and misjudged client demand.

Retail experts like you subscribe to the Weekly EDIT for much more info-backed insights delivered straight to your inbox.